Last Updated on June 16, 2026 by Mike Faremouth, EA, MBA, BSEE – Email Mike

The Benefits of Setting Standards for Business Performance

Introduction:

This may be a dry or dull topic for many – The Benefits of Setting Standards for Business Performance. But, I find these topics enlightening, and anything that gives owners better insight as to their business’s performance is something I’m willing to devote my time and energy to.

So, Let’s begin. What are standards? Many companies have standards and standard operating procedures (SOP’s) that are used to create consistent methods and practices to address many activities like jobs, projects or tasks. These are also monitored, as a feedback mechanism to understand what works, what doesn’t and what needs to be improved. In this short article, I’m going to narrow my focus to operating standards with examples for both product and service providers. Standards are (my simplified definition) edicts, procedures or rules that a business uses that identify those core resource components – labor, material, and all activities and the quantity of each required to produce and deliver one unit of product or service to their Client/Customer.

For manufacturers, this breakdown is usually configured in a usage profile – like a bill of material (BOM) that identifies those core components and the amounts of labor, material, and activities required to complete (and deliver) that product or service.

Setting standards are (what I would consider) and should be a part of Key Performance Indicators (KPI’s) that help business leaders gauge and monitor performance by highlighting variances to expected results and provide the those details to enable corrective actions.

Standards can also extend beyond what I’ve just described here because different customers could have different needs – logistics, being one example. Think about delivering the same parts to an end-item manufacturer (one that assembles finished goods on a dedicated assembly line) vs. delivering these same parts to an original equipment manufacturer (OEM) that requires sequenced deliveries because they batch assemble different finished goods that share the same assembly line or process. One Customer could have much different labeling or packaging requirements from another even though it’s the same part. This could create different standards (for logistics, alone) because of the dissimilar activities involved that create the sort of value that different Client’s or Customers require.

Service providers could also apply standards as well. As an example, different customers for an automotive detailer could have much different expectations as to quality when the detailer processes a bulk number of vehicles through its’ operation. If the detailer offers “good,” “better,” or “best,” options, the detailer and the customer could have very different expectations or opinions as to what constitutes good, better, or best when the job is completed. Sure, this example has more to do with managing expectations than setting standards, but having a set of well-defined standards makes it more difficult for Clients or Customers to argue that their expectations were not met.

Why Setting Standards for Business Performance Matters – Some Examples:

Example #1 (Process Variance)

A small manufacturer that produces identical gaskets for vehicle engines and transmissions, has a standard that 100 pounds of a rubber compound will yield 500 gaskets minus a certain percentage of expected fallout for waste or set-up before the tool is run. If the yield falls below the expected amount, then the process (including material quality) should be investigated so that further yield shortfalls do not occur. If the tool encounters process issues, and fallout rates increase so that in now takes 125 pounds of compound to make 500 gaskets, this business could lose a substantial amount in raw material if it doesn’t monitor yields. A trackable KPI that monitors yields would alert floor personnel to identify the problem(s) and correct the root cause issue.

Example #2 (Build Variance)

Bills of Material or BOM’s are routinely used to assemble parts, sub-systems or finished goods. An assembly process could be reviewed on a monthly (or quarterly) basis by comparing the (period start) balance of components and raw materials, less the sum total of the amounts consumed by the assembly processes for all parts built during this period and comparing that to the actual balances of components and raw materials at period end. Again, allowing for a percentage for scrap and waste (based on historical practice and data) the comparison of actual balances versus expected balances should be close for processes within certain (statistical) limits.

A simple KPI would enable this firm to monitor variances and flag those that occur outside established limits based on historical data. Labor variances could also be calculated by noting any deviation between the actual amount of labor used versus an expected amount. The amount of labor time variance is then translated to a cost variance.

Example #3 (Cost Variance)

If a purchasing agent routinely buys components or raw materials and the price of these components/raw materials increases beyond an expected amount (say, the cost of inflation), then leadership could ask, 1. How much does this cost increase impact our yield – because paying the same amount buys less, so the operation produces less and (as a possible corrective action), 2. Is quality adversely affected if, lower grade components or raw materials are available and used in place of the current grades? The resultant lower yields, based on higher priced inputs gives rise to a possible alternative solution – can lower grade (less expensive raw materials) be used without sacrificing quality? More specifically, what amount of degradation in quality would be acceptable? This cost in quality (including possible service and warranty claims) would need to be evaluated against the savings in raw material costs.

These are just three examples of the benefits of setting standards for monitoring variances in a manufacturing setting. Additionally, standards could be used to understand changes in expected performance resulting from investments in capital or labor for improvements.

Standards could easily be applied to service providers as well. One example would be tracking labor-hours for transport providers. Labor-hour standards could create expected delivery standards (an expected number of deliveries including mileage driven). Standards are more easily set for recurring (weekly) deliveries to customers, and these “milk run,” routes should be chosen to minimize transit time. You could also randomly compare expected transit times with actual transit using a number of GPS tools to capture actual transit time.

The idea here is not to micromanage your staff, just the opposite. It’s to inform leadership when variances occur (either in efficiency, cost or both) that impact processes and operations, so that corrective actions can be applied with the help from staff. It’s not about blame, it’s about arresting problems and fixing them before they become more difficult to address and resolve, later.

Problems, unresolved, become more difficult to address and correct later, because inertia often sets in and change becomes more difficult to implement as staff and workers become accustomed to doing things a certain way. With enough inertia, these sub-optimal ways of doing things could even become standards, themselves? More on this later, under the Some Final Points section.

Efficiency and Cost Variances Explained:

Efficiency variances – most often related to how well labor is utilized, can be expressed as deviations of time (actual vs. expected). Additional examples include, the number of parts produced (actual vs. expected), or the number of tables (turned-over) for a busy restaurant.

Cost variances are deviations from an expected cost vs. an actual cost. Most manufacturers budget for inflation. But, when costs for raw materials, components or delivery/logistics charges (pushed by higher energy costs) exceed budgeted costs, these (unfavorable) variances hit bottom-line profitability. This negatively impacts the expected profit target for the current period – creditors and investors don’t like “surprises.” This is even more problematic when these same manufacturers or service providers lack the ability (pricing power) to offset higher costs with higher prices if doing so, negatively impacts demand/sales.

Cost Variances that Drive Efficiency Variances:

Efficiency variances drive cost variances, that’s intuitive, but take a look at Example #3, above. This is an example of an adverse pricing variance that impacts an efficiency variance because price could impact yields.

Lower yields reduce efficiency because it will take more tool setups and runs to produce an equivalent number of parts. Internally, within a large and complex plant, this will require re-balancing of resources if processing and assembly times increase for those activities affected to produce the same number of parts. This would necessitate an increased need for cross-training workers on multiple operations for the flexibility needed to address this problem.

Further – Why is This Important?

Ok, So what. Why is this so important? Give me a minute and I’ll make my point. Statistically speaking, every operating activity, like a plant, large or small or every service operation, from the simplest to the most complex is unique in that each operation’s inherent performance can be modeled with statistical measures. These measures can also show when an operation (any operation) is outside pre-determined limits based on an accumulation of data.

If you don’t measure performance, you can’t make improvements to your operation – it’s that simple – I’m paraphrasing a famous quote from Peter Drucker. Without calculations or metrics, how would you even know if hiring more employees, making additional investments in labor saving tools or adding some simple automation was worth the cost – if you don’t bother to make before and after comparisons? If you measure performance but don’t take corrective actions when the data tells you, you have a problem, that’s equally as bad.

If you don’t place limits on how your organization functions, your costs will spiral. Another point – consistent performance measures track deviations to expected results that may occur that are outside certain operating limits. Having a robust Management Decision System in place enables leadership to monitor performance over time for potential quality concerns or operating issues.

Moreover, metrics and models reflect and represent the activities and functions of an organization. Organizations evolve and change (over time) particularly under challenging or difficult circumstances. Models need to be inherently flexible when these activities change so that comparisons can be made and correct decisions can be drawn.

One last point. Standards should only be set for those items that are significant (in value) and that are prone to large variations from expected results. Even for a small manufacturer, it’s not worth the cost, effort or time to track most of the items they need to manage. More complex firms could use either a “cutoff” (yes track/no track) value or an impact score (high/medium/low) that an item has to their overall operation in making a determination of which items to track.

Variance Analysis – Two Examples:

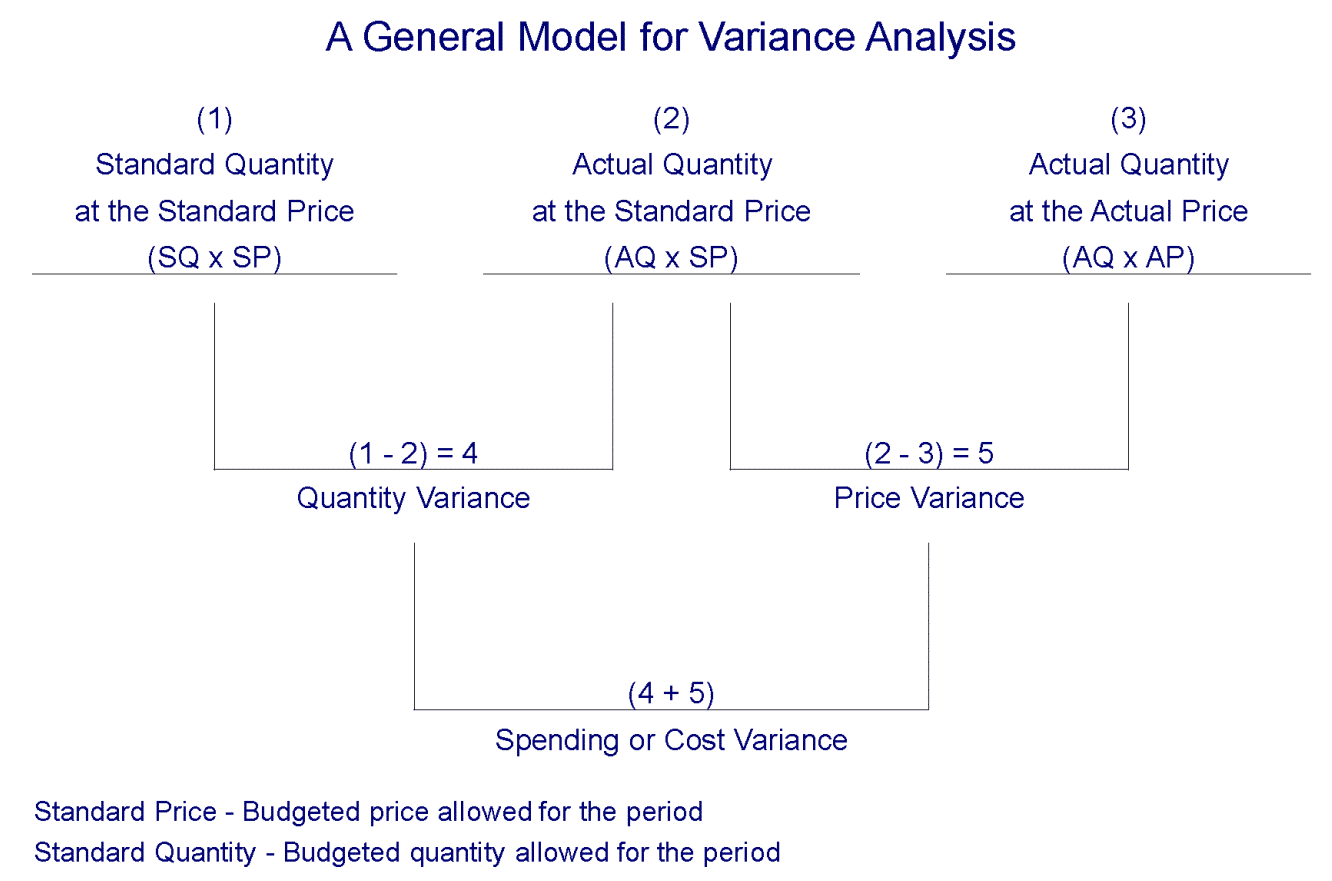

I’m making no attempt to rehash well-known Accounting formulas – this is not an Accounting textbook. I simply want to show some examples. Here’s one – for Direct Materials to explain Cost Variances, Price Variances and Quantity Variances and how each of these relate to each other.

- Cost Variances = Price Variances + Quantity Variances.

- Price Variance = (Std. Price/unit – Actual Price/unit) x Actual Quantity in units or (SP – AP) x AQ.

- Quantity Variance = (Std. Quantity in units – Actual Quantity in units) x Std. Price/unit or (SQ – AQ) x SP.

Example – Jetson Book Publishing

Jetson Book Publishers has standards for the amount of paper used and price per unit of paper. To best illustrate this example and simplify the calculation, each book produced is the same size with an identical number of pages (the latest edition of a very popular book). Paper costs comprise the single largest expense in making a physical book – Book Riot, November 27th, 2018.

- Standard Quantity – The paper content of each book is 1 pound.

- Standard Price – $4.25 per pound, a somewhat higher quality paper stock.

Jetson produced 175,000 of these books in 2022. They used 183,000 pounds of paper and paid (on average) $3.90 per pound.

- Price Variance = (SP – AP) x AQ = (4.25 – 3.90) x 183,000 = $64,050. This variance is favorable because the actual price is less than the standard price.

- Quantity Variance = (SQ – AQ) x SP = (175,000 – 183,000) x 4.25 = $34,000. This variance is unfavorable because Jetson used more than the standard quantity of 175,000 pounds that should have been used to manufacture 175,000 books.

- The Cost Variance is the combination of the Price and Quantity Variances. CV = PV + QV = $64,050 favorable + $34,000 unfavorable = $30,050 favorable.

This analysis can be repeated for labor to understand how well Jetson utilized their direct labor (standard quantity used versus actual quantity) and the price for labor (standard price versus actual price). Again, these actual costs would appear as part of Cost of Goods Sold and any variance would show as part of Jetson’s Management Dashboard for cost variances. Graphically, This analysis is represented below – adapted from Standard Costs and Variances – Chapter 10.

Interpretation – Jetson Book Publishing

Jetson had an overall favorable cost variance (for paper) for this particular book of $30,050. These actual costs are reflected in Jetson’s Cost of Goods Sold (COGS) on their Income Statement. But, these variance calculations are part of Jetson’s (separate) “Management Dashboard,” Key Performance Indicators (KPI’s). Jetson’s favorable variance is in comparison to the standard price and quantity it set as part of it’s budget for raw material – paper, in this example. Setting standards is part of the overall budget process that is (usually) completed before the start of a new period – a fiscal or calendar year.

There are a couple of important distinctions to be made on the use of traditional financial statements versus Management Decision reports like KPI’s. An Income Statement tells the reader nothing about performance versus budget. Usually, Income Statements are compared to prior periods (actual results in the current period versus actual results in the prior period).

Another Example – Labor Variance – Peter’s Construction

Peter’s Construction Company regularly does jobs involving landscaping and fence installation for large commercial properties. A manufacturing firm contacted Peter’s and hired them to landscape and install fencing on a large 1.5 acre warehouse lot.

Peter’s standards estimate that the entire job will require 10 employees and take 17 days to complete at 9 hours per day or 1,530 labor-hours. Peter’s has a standard rate of $26.00 per hour which includes the cost of fringe benefits.

The actual figures for the completed job are: actual rate – $31.07, actual quantity of labor used – 1,887 labor-hours. The price and efficiency variance calculations are straightforward:

- Price Variance = (SP – AP) x AQ = ($26.00 – $31.07) x 1,887 = $9,567.09, unfavorable.

- Quantity Variance = (SQ – AQ) x SP = (1,530 – 1,887) x $26.00 = $9,282.00, unfavorable.

- Cost Variance = $9,567.09 unfavorable + $9,282.00 unfavorable = $18,849.09 unfavorable.

Interpretation – Peter’s Construction

Assuming Peter’s uses a project-based tracking tool, this overall unfavorable variance of $18,849.09 would show as negative variance against the budgeted cost of labor which created the original estimate and (most likely) the contracted cost of labor that was agreed to by the warehousing customer. The cost of labor increased by $18,849.09 compared to the original estimate and the Gross Profit of this job is reduced by $18,849.09 compared to the amount Peter’s had budgeted.

Of course, if the customer requested changes from the original scope of work that required additional labor, then the standards should be revised to reflect these changes in this warehouse job’s Profit and Loss Statement.

Overhead Cost and Efficiency:

The application of variance analysis to overhead (indirect costs) is handled similarly for direct costs like direct labor and material. More importantly, indirect costs/overhead present a unique set of issues when it comes to the accuracy of data in decision support systems for small business managers and owners. Indirect costs and activities that generate cost that are not easily “binned” against the creation and delivery of products and services are often relegated to the “dustbin” of overhead. In many cases (and why this continues to occur is a mystery to me), pre-determined overhead rates are used to “allocate” these costs to products and services.

Often, direct labor hours consumed by the job or project are used to parse indirect and overhead costs. Other methods are also used and this paragraph could easily become an article (or book) unto itself as there are many examples.

Linking indirect activities (that generate indirect costs) to the job or project is a far superior way to create more accurate cost models for every product and service. Allocating costs using methods that don’t consider the link to activities (General and Administrative Costs, for example) that generate cost, will always be inferior and lead to potential costing problems and by extension, possible pricing issues. In one instance, costs could be overstated leading to lost bids (if pricing is based on overstated costs) or lost profits, if costs and pricing are understated.

I’ll tackle this topic in future articles, but if you want a great resource, please see the Profitability Analytics Center of Excellence for more information. PACE devotes a great deal of energy and expertise to help educate (the accounting profession and others) of the pitfalls using conventional financial accounting methods/systems and shortcuts like pre-determined overhead rates.

Why Traditional Financial Statements are Ineffective as Management Decision Tools:

An Income Statement can be modified to compare actual results to budget, but Income Statements are summaries of Account balances that don’t provide the level of detail for Management to (further) investigate or act on favorable or unfavorable variances. So, for example, if the actual costs for raw materials were unfavorable versus budget on a Profit & Loss vs. Budget Statement, the reader would not know which raw materials were creating a problem.

In the Jetson Book example, paper is one raw material, ink is another, as are binding materials like glue or cover material (for hardcover books). Without the type of (granular) detail that KPI’s provide, Management wouldn’t know where to look, if they saw large actual to budget variances on a (30,000 foot view) Profit & Loss vs. Budget Statement.

Another distinction. Income Statements, like all broad performance summaries, are designed to show the reader results of where the business has been, meaning these summaries are backward looking – they show what has happened. These Statements are also cumulative, and aggregate the results from many completed jobs or product shipments. Management Decision reports – like dashboards or KPI’s are created to show (not only) what has happened but to provide a level of detail – a mechanism for control, so that Management can act. These reports are specifically designed for Management to take action if they see results that differ from the standards they set at period start.

Some Final Points:

None of this analysis should be done without accurate, consistent data. Consistent data means that the methods used to calculate or create the data should be the same (over time) to ensure that the same results and the same conclusions can be drawn.

Without accurate and consistent data, these calculations will likely be incorrect – inaccurate data will yield results that will not be realistic and any decisions made may be erroneous. Same as with inconsistent methods. A calculation may suggest an unfavorable variance, when in fact, it’s favorable.

Standards are best set using time studies, and budgets that are set prior to the current period, should take into consideration economic factors, such as inflation that will affect the cost to obtain inputs to operate the business.

Lastly, and probably most important, standards will only be relevant and adopted/used by organizations if they are realistic, and well-intentioned. If they are not used as a means to positively reinforce an organization’s goals or mission but seen merely as punitive, biases and tampering will likely occur and compromise the effectiveness of these performance tools.

Comments? Disagreements? Please leave in the Comment Section below this article or write to me at mike@easllc.co. You can also Contact Us Here.

Social Sites / On Google Maps:

Find us/Follow us on: